|

|

|

|

Unless a S381 election is made by both parties, balancing adjustments do not arise on the transfer of an agricultural building. The former owner's annual allowance in the period of the transfer is time apportioned.

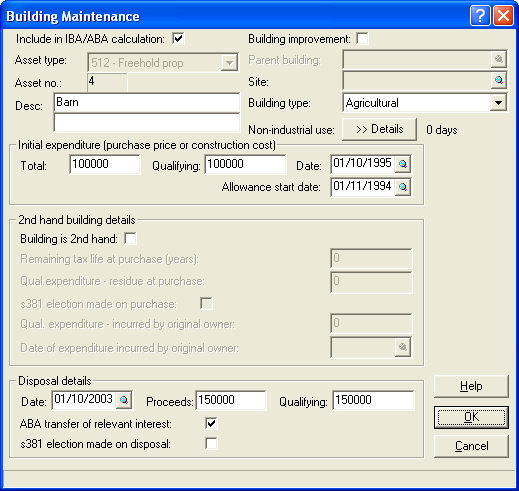

Example data

A owns a barn which cost £100,000 on 1 October 1995.

The barn is sold to B on 1 October 2003 for £150,000.

A's accounting period end date is the 31 October.

Business Tax will give A an annual allowance of £3,671 being the £4,000 annual allowance time apportioned by 335/365 days.

Complete the Building Maintenance screen as follows: