|

|

|

|

This topic explains how to enter the details required on the CT600 and

the computation, as per HMRC guidance.

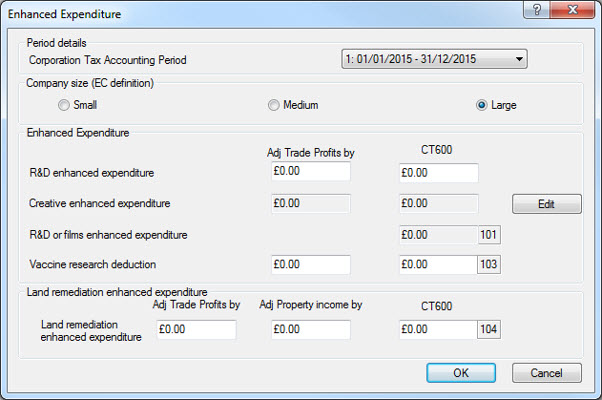

Large company clients may qualify to claim the Research and Development expenditure credit. SME companies can claim Research and Development tax credits, (enhanced deduction).

For businesses with accounting periods prior to the 1st April 2019

This is important, as it is only large companies that can claim ‘above the line’ tax credit. This will also put a X in box 100 of the CT600 (large companies).

The following screen displays.

The following screen displays.

Click Details next to Above the Line tax credit.

On the first tab Calculated Tax Credit the expenditure details are entered.

Box A - Pro rata the qualifying expenditure (pre April 15 and post April 15) as the rate changed in April 2015 from 10 % to 11%.

In order to claim the 49% select the Ring fence trade option.

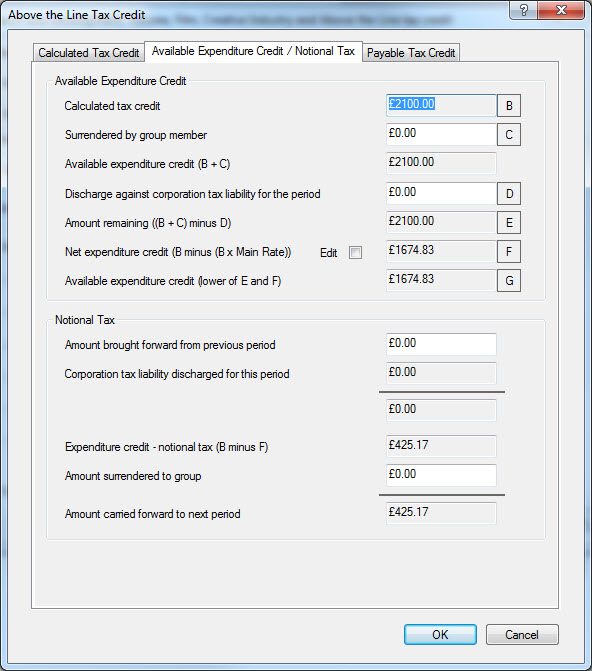

On the second tab Available Expenditure Credit/Notional Tax the adjustments are entered.

Box B - The calculated value Box A x % credit rate.

Box C - Any tax credit surrendered by group members can be entered in here.

Box D - If there is an amount to offset against the corporation tax for the period this is entered in here.

Boxes E, F and G are calculated automatically. If Box F needs to be amended, select the Edit box and change the calculated value.

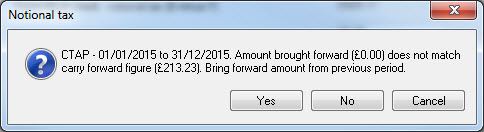

In the Notional Tax section, enter the amount brought forward from the previous period. If an Edit | Bring forward has been done then this will automatically be populated with any amount to b/f.

If the Bring Forward was not run then by clicking in the Amount brought forward from previous period box will trigger a validation to complete this box automatically.

Clicking Yes will enter the value b/f from last year.

Any amount to be surrendered to a group is entered in the Notional Tax section as well.

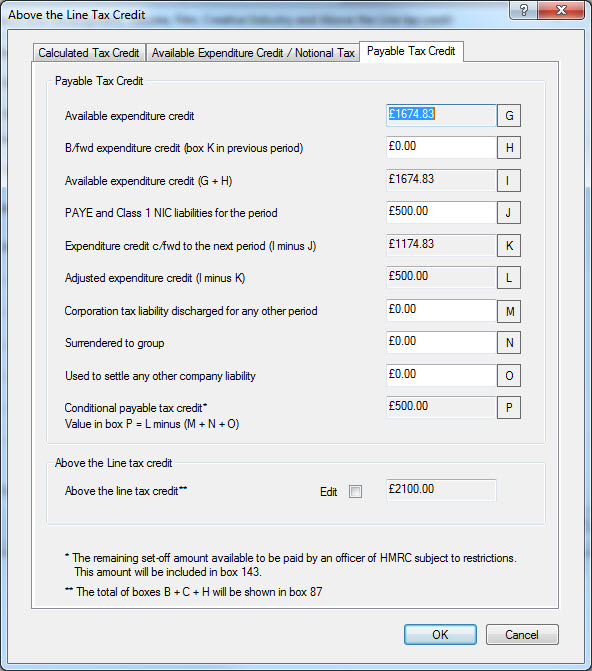

The third tab Payable Tax Credit is for the final adjustments to arrive at the repayable tax credit.

Box G - this is the available expenditure credit.

Box H - this is the same value as Box K in the previous period which is automatically populated when running an Edit | Bring forward.

Box I - calculated automatically.

Box J - enter the PAYE and Class 1 NIC liabilities for the period.

Box K - calculated automatically and will populate Box H in the following year.

Box L - calculated automatically.

Box M - enter any amount to be set off against the corporation tax liability for any other period.

Box N - enter any amount to be surrendered to group.

Box O - enter any amount used against any other company liability.

Box P is the conditional Payable Tax Credit which populates Box 143 on the CT600.

The Above the Line Tax Credit figure at the bottom will populate Box 89 on the CT600 and the figure can be amended if needed by selecting the Edit option. This is also the figure that appears on the corporation tax summary in the computation and is correctly showing according to HMRC guidelines.

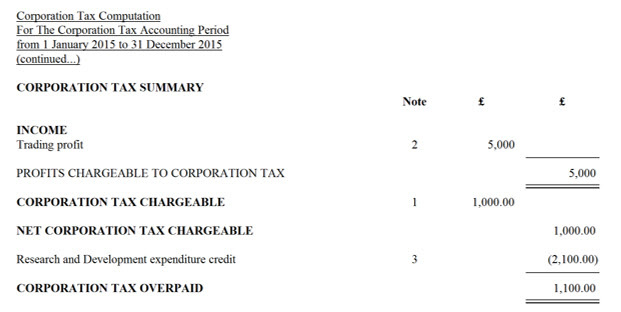

Once the Tax credit has been entered, click Reports | Corporation Tax | Enhanced. The tax credit will reduce the net corporation tax chargeable as shown below. It will also show the break down for the ‘above the line’ tax credit on the computation as a note.

Entering a RDEC (for Accounting periods Starting on or after 1st April 2019)

To access the RDEC screen select either:

Edit | Research and development | RDEC (tab)

Enhanced Expenditure | select Edit next to box 660

Calculation | Tax Reconciliation | select Edit next to box 530

All above location will display the following screen:

Enter the qualifying expenditure – IRIS will automatically calculate the tax credit at the applicable rate. (selecting ‘Ring fenced will calculate the tax credit at 49%).

Enter any RDEC claimed from any group company.

Any outstanding corporation tax liability will be automatically offset against the calculated tax credit.

If RDEC remains, the remaining tax credit will be restricted by the notional tax. (Notional tax is carried forward to the following period and will appear within the ‘Notional tax’ section).

PAYE and NIC paid for the AP will be required to be entered. (Any RDEC in excess of the PAYE and Class 1 NIC will be carried forward to the following period).

The payable tax credit is restricted to the PAYE and NIC class 1 paid for the period.

Enter any remaining corporation tax liability to be discharged from other accounting periods, any tax credit which has been surrendered to a group company or any other outstanding company liability to be offset against the payable tax credit (all these amounts will reduce the final payable tax credit).

The payable tax credit will be displayed in the final field.

IRIS will automatically make an adjustment for the RDEC on the computation. The value that will be added back to the profit/(loss) per financial statements is reflected within the Add back to profit field.

The calculated tax credit will reduce the net corporation tax chargeable as shown below.

A comprehensive break down of the RDEC calculation

will appear on the computation as a note.

For accounting periods starting on or after April 2019

To access the RDEC screen select either:

Edit | Research and development

Enhanced Expenditure | select Edit next to box 660

Calculation | Tax Reconciliation | select Edit next to box 530

The above location will display the below:

Enter the qualifying expenditure within the corresponding field.

IRIS will automatically calculate the ‘Adj trade profit by’ value as well as the enhanced deduction (Box 660).

Enter any PAYE and Class 1 NIC paid within the period, the maximum R&D tax credit that can be claimed is 3 time the PAYE and Class 1 NIC for the period. IRIS will automatically restrict the R&D tax credit.

The tax credit is calculated from taking the tax credit rate and multiplying it by the lower of the ‘unrelieved trade loss and the ‘Enhanced deduction’.

An adjustment will be made on the computation which corresponds to the value within the ‘Adj trade profit by’ field, this value is deducted from the profit/(loss) per financial statements.

An adjustment is also made against the losses to be carried forward, Losses are surrendered in order to claim a payable tax credit.